Rivian’s Q1 2026 shareholder letter dropped today and it is packed. R2 saleable production officially started last week in Normal, customer deliveries are landing in the coming weeks, the Georgia plant got a 50% capacity bump to 300,000 units annually, and the $1 billion Volkswagen Group equity investment tied to RV Tech winter testing milestones hit Rivian’s bank account today. There is a lot to get through.

On the financial side, Rivian pulled in $1.38 billion in revenue, an 11% increase year over year, with deliveries up 20% to 10,365 vehicles. Gross profit came in at $119 million, which sounds rough next to the $206 million from Q1 2025, but the comparison is muddied by a $100 million drop in regulatory credit sales. That kind of swing has nothing to do with how the underlying vehicle business is actually running.

Adjusted EBITDA was negative $472 million. Cash and short-term investments sit at $4.83 billion, with total available liquidity at $5.4 billion when you include the ABL facility. Fold in the $1 billion VW that just landed, the $300 million initial Uber commitment expected to close in Q2, the optional $1 billion VW non-recourse loan in October, and the up to $4.5 billion DOE loan, and you start to see why Rivian is comfortable spending into the R2 ramp without flinching.

R2 production has officially started

This is the moment. Saleable R2 vehicles are being built in Normal. Some have already gone out to employees as the team works through the early ramp, and customer deliveries are expected within weeks. For anyone who has been following the R2 timeline since the SXSW reveal, this is the line that turns it from concept and prototype to a real vehicle in real driveways.

R2 Performance launches first this spring with dual-motor AWD, 656 horsepower, and an EPA estimated range of up to 330 miles. R2 Premium follows late this year at 450 horsepower with the same 330 mile estimated range. R2 Standard, the long-range RWD configuration, lands in the first half of 2027 with 350 horsepower and a Rivian estimated 345 miles. The roughly $45,000 Standard variant everyone has been asking about is still slated for late 2027, which lines up with what Rivian has been saying for a while.

So if you are holding out for the cheapest R2, that wait is real. If you want one this year, Performance is the way in.

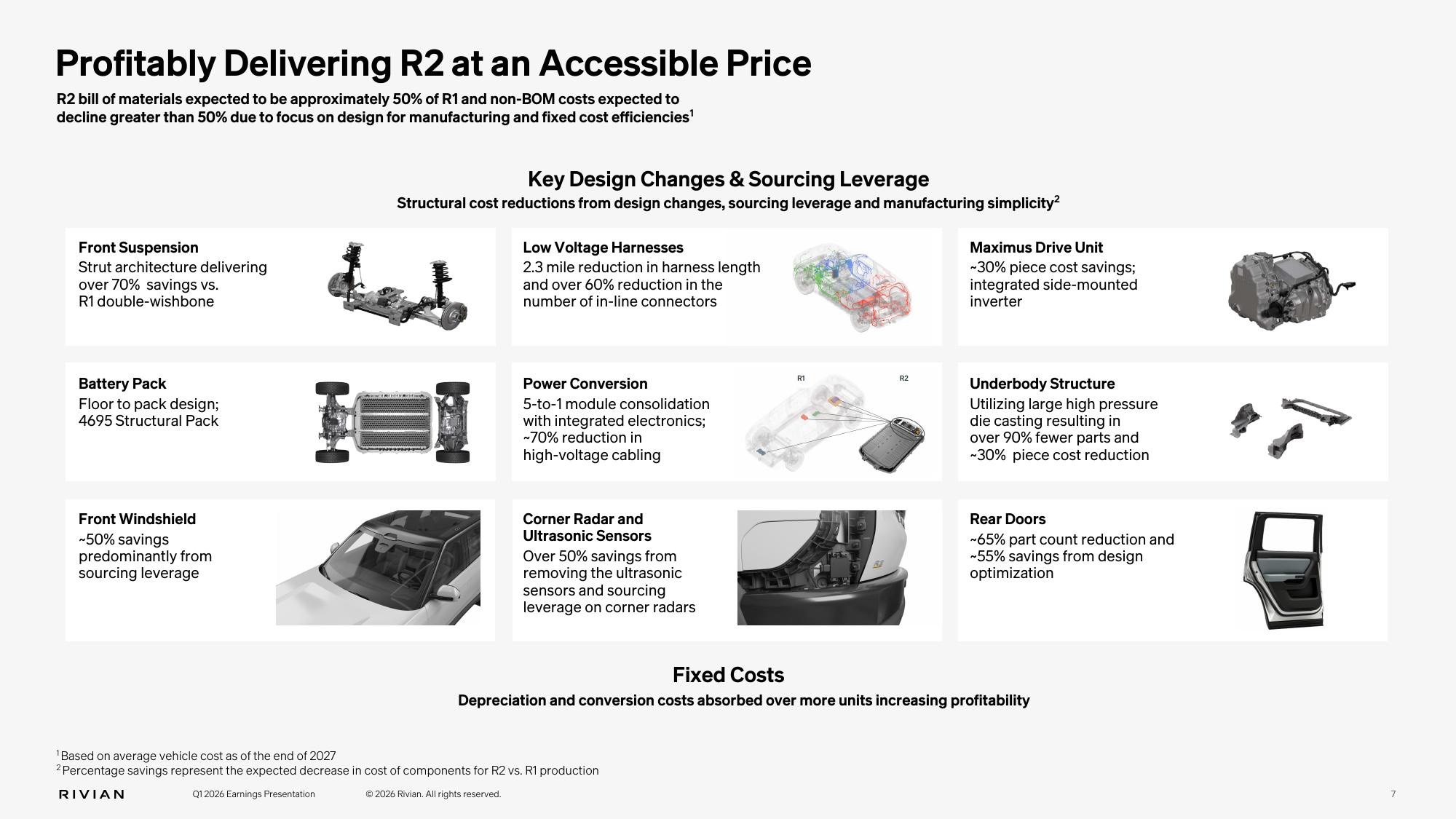

R2 cost structure is the actual story

Buried in the PDF is a slide on R2 component-level cost reductions and this is where the long-term math lives. Rivian expects R2’s bill of materials to come in at roughly 50% of R1, with non-BOM costs declining by more than 50% as well.

Some of the highlights. The front suspension moves from a double-wishbone setup on R1 to a strut design on R2, saving over 70%. The new Maximus drive unit with an integrated side-mounted inverter delivers about 30% in piece cost savings. The underbody uses a large high-pressure die cast structure that has over 90% fewer parts and around 30% lower piece cost. Power conversion got a 5-to-1 module consolidation with about 70% less high-voltage cabling.

The battery is a floor-to-pack design using 4695 structural cells. Low voltage harnesses are 2.3 miles shorter on R2 with over 60% fewer inline connectors. The rear doors alone shed about 65% of part count and around 55% in cost. Even the front windshield is roughly 50% cheaper, mostly through sourcing leverage.

This is the kind of structural cost engineering you need to make a $45,000 EV actually profitable. R2 was never going to be R1 with a smaller body. It was always going to be a fundamentally different cost platform, and this slide makes that pretty obvious.

Georgia gets bigger, the DOE loan gets smaller

This one is interesting. Rivian increased Phase 1 capacity at the Georgia plant by 50%, from 200,000 units annually to 300,000 units, while at the same time restructuring the DOE loan from up to $6.6 billion down to up to $4.5 billion. Production is still expected to start in late 2028 and Rivian now plans to draw on the loan by early 2027 once conditions are met.

So the headline reads two ways depending on which one you pick up. The TechCrunch crowd will frame it as a downsized loan. The other read is that Rivian is getting more capacity per dollar of debt, which is arguably the better outcome for shareholders. Less leverage, more output, same timeline.

The new $4.5 billion package is $4,006 million in principal plus $494 million in capitalized interest. Future phases of the Georgia plant are still on the table but would need separate financing if they happen.

A 50% capacity bump before the plant has even opened is a confidence signal worth noting. It also helps the unit economics. Stretching depreciation and conversion costs across more vehicles is exactly how you wring margin out of a manufacturing platform, and it is how Rivian eventually gets R2 to pay for itself.

Volkswagen and Uber are funding the next chapter

RV Tech, the joint venture with Volkswagen Group, completed winter testing of its production-intent zonal architecture for the first generation of VW software-defined vehicles. Testing happened in Phoenix and Arjeplog, Sweden, with joint teams from Volkswagen, Audi, Scout, and RV Tech. That milestone unlocked the next $1 billion equity investment from VW, which Rivian confirmed it received today.

Another $460 million from VW is expected at the earlier of the first VW vehicle with RV Tech hardware on the road or January 2028. There is also the optional $1 billion non-recourse loan available to Rivian in October.

On the Uber side, the autonomous partnership announced in March is moving forward. The total commitment is up to $1.25 billion through 2031, with $300 million expected to close in Q2 2026 at signing, $250 million tied to a milestone by end of 2026, and up to $700 million more across milestones running through 2031. There is also the vehicle commitment for up to 50,000 fully autonomous R2 robotaxis and software licensing fees tied to Uber’s use of Rivian’s Level 4 system.

Not small numbers, and they come with actual dates and milestones attached. The point is liquidity, and Rivian has the runway it needs.

Software and services keeps quietly outperforming

Software and services revenue jumped 49% year over year to $473 million, with gross profit of $181 million at a 38% margin. Most of that growth comes from RV Tech vehicle electrical architecture and software development services, plus higher repair, maintenance, and remarketing.

This segment used to be a rounding error. Now it is doing real work in the income statement and it is the part of the business that is consistently profitable, which is something most EV companies cannot say about anything.

Mind Robotics and ALSO continue to fund themselves

Mind Robotics closed a $500 million Series A co-led by Accel and Andreessen Horowitz, with Rivian holding around 38% on a shares outstanding basis. Rivian recognized a $506 million gain in the quarter from the Mind Robotics deconsolidation tied to that round, which is the line item showing up in “other income” if you are reading the statements directly.

ALSO closed a $200 million Series C led by Greenoaks with Prysm and a strategic investment from DoorDash, plus a multi-year commercial agreement with DoorDash to deploy small purpose-built EVs for last-mile delivery. Amazon also signed on to buy thousands of TM-Q pedal-assist cargo quads from ALSO. Rivian holds around 35% there.

The spin-out strategy is starting to look like a real second pillar instead of just an accounting curiosity.

Service network is keeping pace

Rivian crossed 100 service centers in the quarter, with 39 Spaces, 145 Adventure Network locations, 973 chargers, and over 680 mobile service vans on the road. Service infrastructure tends to be the part nobody pays attention to until they need it, but with R2 about to multiply the customer base, this is going to matter a lot more than the headline numbers suggest.

The 2026 R1S also got Top Safety Pick+ from IIHS, which is the kind of credential that quietly closes a lot of family driveway decisions.

Guidance

Rivian is guiding 62,000 to 67,000 deliveries for full year 2026, with adjusted EBITDA of negative $1.8 to $2.1 billion and capital expenditures of $1.95 to $2.05 billion. The delivery range bakes in the early R2 ramp without being overly aggressive, which is probably the right call given how every automaker tends to slip on first-year volume targets for a new platform.

The full Q1 2026 earnings letter is available through Rivian’s investor relations page for anyone who wants to dig through the slides directly.

The R1 era is not over, but Q1 2026 is the first quarter you can clearly see the R2 era starting to take shape underneath it. The next two quarters are where the actual ramp gets tested, and that is the part nobody really knows how to model yet.