Rivian is building something that looks a lot bigger than “just” a better driver assist system. If you zoom out, the real product is the full autonomy pipeline, the in-vehicle compute, the electrical architecture that ties it all together, and the tooling to ship updates safely at scale. That is exactly the kind of stuff legacy automakers keep tripping over, and it is why Rivian is in a pretty unique position to sell pieces of its autonomy platform to other brands.

The “why” starts with money, and margin. Building autonomy is brutally expensive, and the best way to make that math work is to spread R&D across more vehicles than you personally sell. A licensing or platform business lets Rivian monetize its software and electronics as a high-margin stream, which is also very aligned with where the industry is going (software-defined vehicles, fewer ECUs, more centralized compute). Volkswagen’s joint venture with Rivian is already centered on a next-gen zonal architecture and software stack for future vehicles, and VW has publicly talked about progress, reference vehicles, and testing timelines, which is basically a public validation that Rivian’s underlying approach is valuable to a much larger OEM footprint.

tl;dr

- Licensing the platform helps spread R&D costs and creates high-margin software revenue.

- Legacy automakers struggle with vehicle software, making Rivian’s architecture attractive.

- The Volkswagen joint venture validates real OEM demand for Rivian’s tech.

- Rivian can license in layers, from vehicle software and ADAS to autonomy compute.

- Autonomy+ shows Rivian already knows how to package and support software.

- Validation, simulation, and safety tooling may be Rivian’s most valuable offering.

- Liability, regulation, and OEM customization remain the biggest challenges.

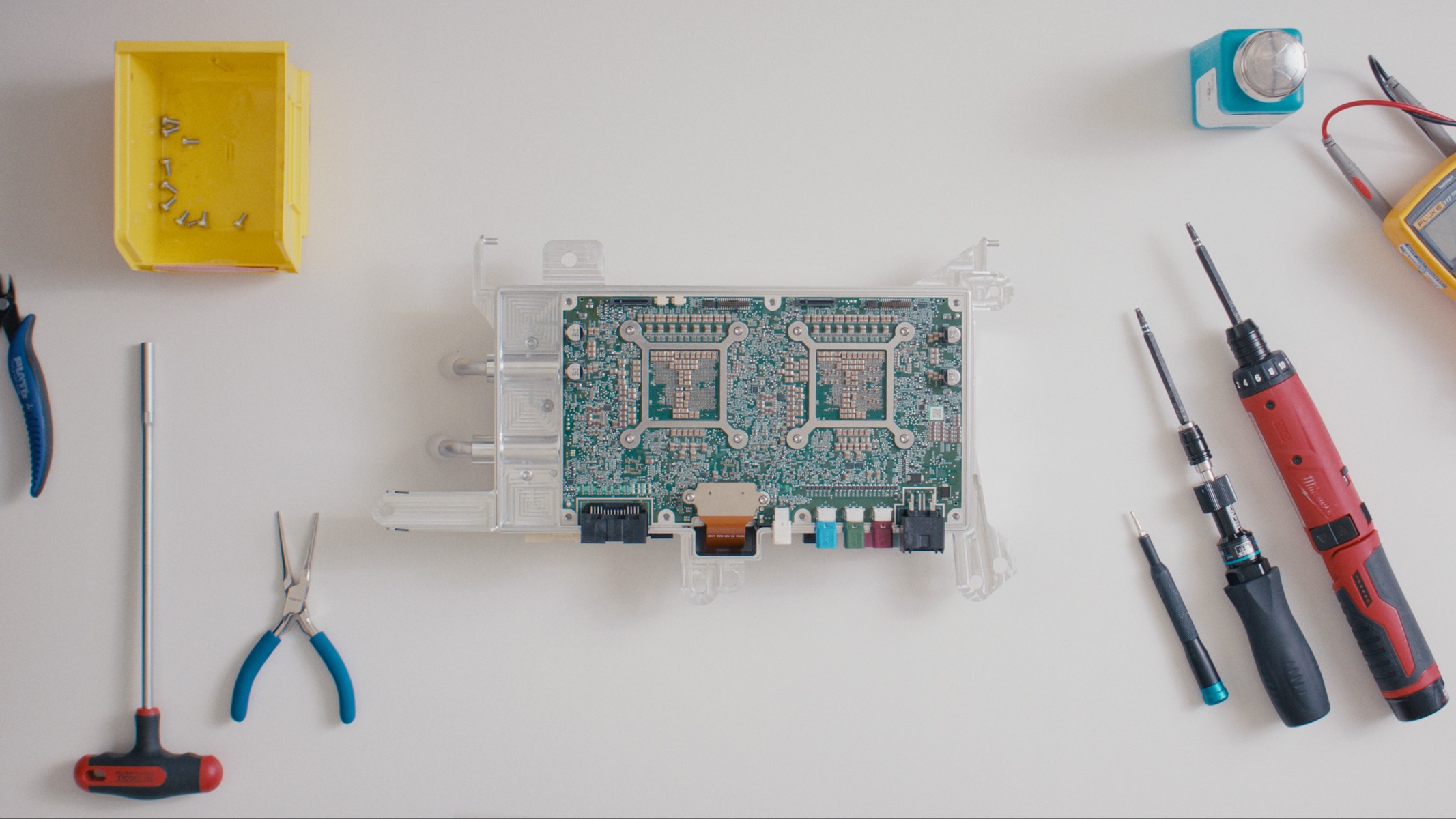

There is also a “timing” reason. Rivian just put big stakes in the ground at Autonomy and AI Day: custom silicon (RAP1), a next-gen autonomy computer, and a broader autonomy platform roadmap. That is the kind of vertical integration that makes licensing more compelling, because you are not only selling an app, you are selling a full, tuned system where hardware and software were designed together.

And importantly, there are signals this is not hypothetical. Reuters reported earlier in 2025 that Rivian said other automakers were “knocking on the door” about technology coming out of the VW joint venture.

Now the “how”, and this is the fun part, because Rivian would not need to sell one monolithic “Rivian Autonomy” product. The most realistic path is modular, with clear tiers.

They could sell the foundation first (the piece everyone needs before autonomy even matters): the electrical and software architecture. That includes the zonal approach, the vehicle network, how modules talk to each other, the OTA update pipeline, diagnostics, and the safety and redundancy patterns. This is already the core of the Rivian-VW JV focus, and it is attractive even for automakers that are years away from anything resembling hands-free driving.

Then they could offer the ADAS layer as a packaged “bring-up fast” option. Think: lane centering, adaptive cruise, lane change on command, hands-free on supported roads, plus the driver monitoring and attention system that makes regulators and safety teams less nervous. Rivian is already productizing this as Autonomy+ with a clear pricing model for consumers, which is a hint they are learning how to package and support a software product at scale.

After that, they could license the autonomy compute and perception stack as a reference design. This is where RAP1 and the Gen 3 compute direction matters. An automaker could buy a proven compute module (or a spec they can manufacture/dual-source), paired with Rivian’s compiler toolchain and runtime, and a validated sensor suite recipe. If the platform is designed to be “drop-in enough”, it saves other OEMs multiple years of integration pain.

Finally, they could sell the hardest part as a service: validation, simulation, and safety case tooling. Autonomy is not “did the demo work”, it is “can you prove it works across weird edge cases and ship updates without breaking compliance”. If Rivian builds internal tooling for data labeling, scenario mining, simulation regression, and release gating, that becomes extremely sellable to any automaker that is drowning in software QA for vehicles.

If Rivian really wanted to push it, there is an even more ambitious version: become a supplier-like platform where multiple automakers feed anonymized driving data into a shared improvement loop, then each brand gets tuned outputs (different driving style, different feature set, different geofencing rules). That is tricky politically and legally, but it is how you create a compounding advantage.

Of course, there are real obstacles.

Liability and brand risk is a big one. If an automaker licenses Rivian tech and a crash happens, lawyers will still drag everyone into the room. That means Rivian would need very clear contracts, strict operational design domains, strong driver monitoring requirements, and likely a model where the automaker owns the final calibration and release sign-off.

Differentiation is another. Automakers do not want to feel like they are buying the same soul as their competitor. So Rivian would need to let partners customize UX, driving behavior tuning, feature bundles, and even compute levels, while still keeping the platform supportable.

Regulation and data privacy are the slow-burn issues. Cross-OEM data sharing is complicated, and different regions will have different rules. This pushes the business toward either (1) on-prem and per-OEM data silos, or (2) very carefully designed anonymization and aggregation.

My take: Rivian does not need to become “the Android of cars” overnight to win here. The smartest path is selling the picks and shovels first, the zonal architecture, the OTA and vehicle software platform, the validated autonomy building blocks, then letting automakers climb the ladder as trust builds. The VW JV is basically a giant proof point that this can work at scale, and if other OEMs keep struggling to modernize, the line at Rivian’s door probably gets longer.

Nice and concise presentation.